Why Businesses Get Labeled “High-Risk” – And Why Most Merchants Don’t Understand the Payment Industry’s Hidden Risk Model

- June 15, 2026

- Soham Guchait

Many business owners are surprised the first time they hear their company described as a “high-risk merchant.” The term often creates the impression that a business is doing something wrong and operating in a questionable industry. In reality, that assumption is often far from the truth.

Some of the world’s most legitimate businesses—including travel agencies, subscription services, online marketplaces, gaming platforms, forex providers, and digital content companies—are routinely classified as high-risk by banks and payment processors. The label has less to do with a company’s reputation and more to do with how the payments industry evaluates financial risk behind the scenes.

Understanding this hidden risk model is important because it directly affects a business’s ability to accept payments, access merchant accounts, control processing costs, and scale internationally. Yet most merchants never receive a clear explanation of why they have been categorized as high-risk in the first place.

The Biggest Misconception About High-Risk Businesses

One of the most common misconceptions is that high-risk businesses are inherently unsafe or unreliable. In reality, payment providers use the term as a technical classification rather than a moral judgment.

A business can be highly profitable, legally compliant, and widely trusted by customers while still being considered high-risk from a payment processing perspective. The classification simply means that the processor believes there is a greater chance of financial loss associated with handling that merchant’s transactions.

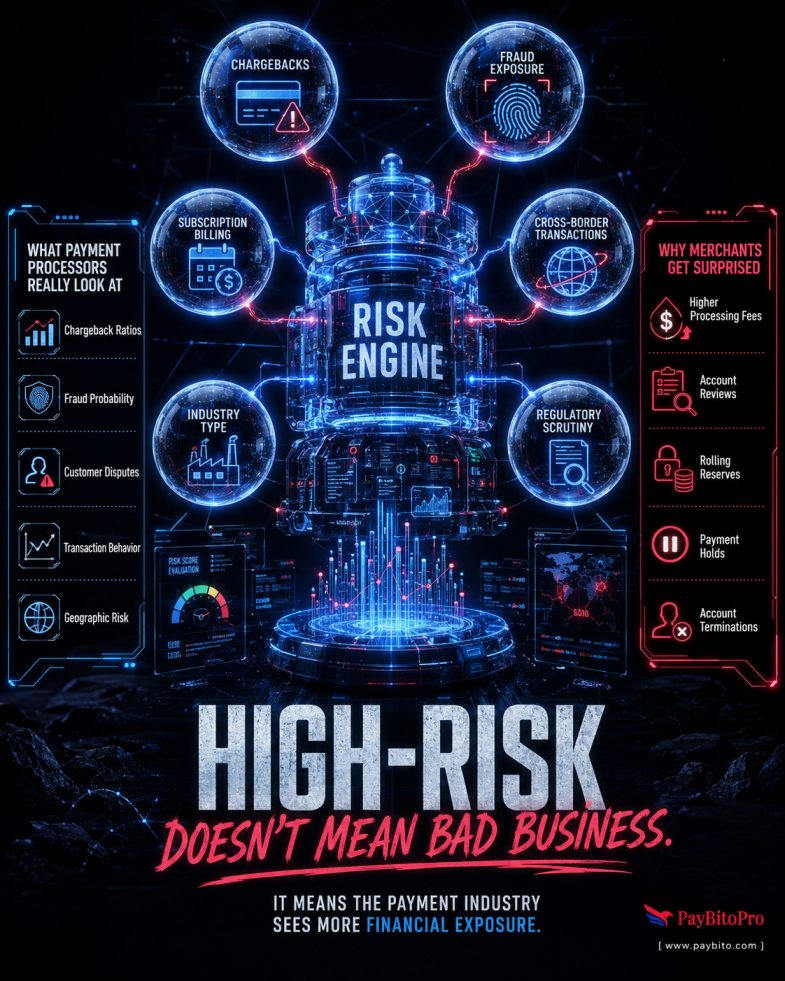

For example, industries that process recurring payments often experience higher levels of customer disputes. Businesses operating internationally may face increased fraud exposure due to cross-border transactions. Companies selling digital products can encounter challenges because products are delivered instantly, making disputes harder to resolve. None of these factors indicate that a business is problematic, but they do influence how payment providers assess risk.

How Payment Processors Actually Measure Risk

When a merchant applies for payment processing, providers analyze a wide range of factors that go far beyond revenue or company size.

Chargebacks are among the most important considerations. A chargeback occurs when a customer disputes a transaction through their bank. Excessive chargebacks can create financial losses for payment processors and acquiring banks, making them cautious about merchants with elevated dispute rates.

Fraud exposure is another major factor. Certain industries naturally attract more fraudulent activity because of their customer demographics, transaction patterns, or digital nature. Businesses operating in sectors such as online gaming, digital subscriptions, and international e-commerce often face heightened scrutiny for this reason.

Transaction volume and average ticket size also play a role. Large or sudden increases in payment volume may trigger additional reviews because processors monitor unusual activity that could indicate fraud or operational instability. A business processing thousands of transactions per day presents a different risk profile than one handling a few hundred.

Geographic exposure further complicates the picture. Merchants serving customers across multiple countries must navigate different regulations, currencies, fraud patterns, and banking environments. While international expansion creates growth opportunities, it also introduces additional layers of risk that processors must account for.

Why Two Similar Businesses Can Receive Different Processing Terms

One of the most frustrating realities for merchants is that two companies operating in the same industry can receive completely different payment processing offers.

The reason lies in the details. A business with strong customer support, transparent billing practices, clear refund policies, and a history of low chargebacks may be viewed more favorably than a competitor selling similar products.

Payment providers increasingly rely on sophisticated underwriting models that evaluate merchant behavior, transaction history, customer complaints, and operational stability. This means that risk assessments are often based on a combination of industry classification and individual business performance.

As a result, being categorized as high-risk does not automatically mean a merchant will face severe restrictions. Businesses that actively manage risk can often secure better terms and greater processing flexibility.

The Hidden Costs of High-Risk Classification

Many merchants focus primarily on processing fees, but the true cost of high-risk classification extends much further.

Higher transaction fees are common because processors are pricing in additional exposure. Some merchants may also be required to maintain rolling reserves, where a portion of transaction revenue is temporarily held to cover potential disputes or chargebacks.

Account reviews can become more frequent, and onboarding processes may involve additional documentation and compliance checks. In extreme cases, businesses may experience account freezes or sudden terminations if risk thresholds are exceeded.

These challenges can disrupt cash flow, affect customer experience, and create operational uncertainty. For growing businesses, understanding these risks is often just as important as managing sales and marketing activities.

Reducing Your Risk Profile as a Merchant

Although some factors are beyond a merchant’s control, there are practical steps businesses can take to improve their payment processing stability.

Clear product descriptions and transparent billing practices help reduce customer confusion and disputes. Strong customer service can prevent complaints from escalating into chargebacks. Fraud prevention tools, identity verification measures, and transaction monitoring systems can also significantly reduce exposure to fraudulent activity.

Businesses should also regularly review refund policies, checkout experiences, and customer communication processes. Many payment disputes occur not because of malicious intent, but because customers do not understand what they purchased.

The most successful merchants view payment processing as a strategic component of their business rather than a simple backend function. By actively managing risk, they create a stronger foundation for long-term growth.

The Future of High-Risk Payment Processing

As digital commerce continues to expand, the traditional approach to risk management is evolving. Artificial intelligence, machine learning, real-time fraud detection, and payment orchestration technologies are helping processors evaluate merchants with greater accuracy than ever before.

At the same time, businesses are increasingly seeking flexible payment solutions that support global transactions, alternative payment methods, and emerging digital assets. This shift is creating opportunities for specialized payment providers that understand the unique challenges faced by high-risk merchants.

Platforms such as PayBito, which offer payment solutions designed for businesses operating in complex or high-risk environments, reflect this broader industry trend. Rather than treating high-risk classification as a barrier, modern payment providers are focusing on helping merchants manage risk more effectively while maintaining reliable payment acceptance capabilities.

Ultimately, the high-risk label is not a verdict on a business’s legitimacy. It is simply a reflection of how financial institutions assess exposure in an increasingly complex digital economy. Understanding risk helps merchants navigate payment challenges and grow sustainably..

Categories

- AI (9)

- Altcoins (10)

- Banking (11)

- Bitcoin (134)

- Bitcoin ETF (11)

- Bitcoin Price (30)

- Blockchain (50)

- Brokering World Hunger Away (16)

- Business (13)

- CBDC (11)

- COVID-19 (3)

- Crypto ATMs (1)

- Crypto Banking (18)

- Crypto Bill (1)

- Crypto business owner platform (31)

- Crypto Investment (3)

- Crypto Markets (5)

- Crypto Payment (37)

- Crypto Payment Processor (4)

- Crypto Prices (1)

- Crypto Trading (92)

- Cryptocurrency (402)

- Cryptocurrency Exchange (108)

- Data Visualization (2)

- Decentralized Finance (7)

- DeFi Payment (9)

- DEX (3)

- Digital Currency (23)

- Ethereum (2)

- FAQ (7)

- Finance (29)

- Financial Equality (4)

- Financial Freedom (8)

- Forex (25)

- ICO (2)

- Investment (11)

- Mining (3)

- News (66)

- NFTs (2)

- P2P (1)

- PayBitoPro (697)

- PayBitoPro Coin Listing (6)

- PayBitoPro Exchange (2)

- Payment Gateway (22)

- Post COVID Digital Transformation (1)

- Press Release (130)

- Privacy & Security (3)

- Real Estate (1)

- Stablecoin (6)

- Technology (16)

- Uncategorized (3)

- US Presidential Election (2)

- Utility Coin (1)

- Web3 business (4)

- Web3 Wallets (2)

- White Label Crypto Exchange (8)

Recent Posts

- Why Chargebacks Are a Major Threat to Forex Brokers?

- From Dream Vacation to Abandoned Cart: The Payment Mistakes That Drive Travelers Away in 2026

- The Gamer’s Regret: Why Video Game Studios Are Labeled “High-Risk”

- Why Businesses Get Labeled “High-Risk” – And Why Most Merchants Don’t Understand the Payment Industry’s Hidden Risk Model

- The High-Risk Merchant Survival Map: Navigating Payment Challenges in a Complex Digital Economy